Premium

Financing

Plans

Premium Financing Plans on life insurance policies can be a significant expense, especially for larger coverage amounts. For many of our clients, these required premiums are a strain on their ability to maintain their current lifestyle. For these high net-worth individuals, we’ve found that premium financing offers an innovative and effective solution. They can purchase the life insurance they need without liquidating other investments or otherwise changing their normal cash flow, and in many cases, reduce potential estate taxes.

A well-structured premium financing arrangement can help high-net-worth clients secure a significant insurance policy without making a large, out-of-pocket premium payment.

Strategies of Preserving Legacy by Financing Life Insurance Premiums

If you anticipate a need for liquidity upon your death, whether to cover the taxes due on your estate or to facilitate a smooth transfer of your business, a life insurance policy with a substantial death benefit could be a wise addition to your wealth and estate plan. Unfortunately, the premiums associated with such a plan can be significant. You may need to liquidate investments to cover the cost, potentially exposing yourself to gift or capital gains taxes and reducing your ability to take advantage of growth in your portfolio.

There is, however, another way. By borrowing money to pay for the premiums, you may be able to maximize the benefit of the life insurance policy while minimizing your exposure to taxes and leaving your current investment strategy intact.

Are Premium Financing Plans Right for you?

Generally speaking, premium financing is a suitable strategy for those with a net worth of $25 million or greater who wish to use insurance to provide the liquidity necessary to pay estate taxes and ensure that they are able to pass their legacy assets on to their heirs. This strategy serves those individuals who do not want to sell off investments or allocate current income to addressing that need. Whether or not it makes sense in a particular case depends on a number of factors: how much insurance is needed, what the associated costs are and, whether or not there may be alternative estate planning techniques that satisfy the need.

If you are considering this strategy, begin by working closely with your attorney to devise an estate plan. If you decide you need insurance, reach out to a life insurance professional. Trying to determine the appropriate policy can be a complex and challenging undertaking, and a life insurance professional can help you select the policy type and amount that’s appropriate for your situation. Your advisors can also help you determine the ownership of the insurance policy. It’s important to explore all your payment options, based on your individual situation and financial needs. While premium financing may be the right strategy for you, you should first consider if you would be better served by paying the insurance premiums outright.

Because the interactions between the life insurance policy, your estate plan, your investments and the loan are complicated, it’s critical that you work closely with a team of advisors who have experience and expertise in these matters and understand your financial situation. There is not a “one-size-fits-all” optimal strategy when it comes to this topic. Therefore, it’s imperative that your team of professionals can coordinate and work together to help you determine the best choices for you, given the potentially millions of permutations.

How Premium Financing Works?

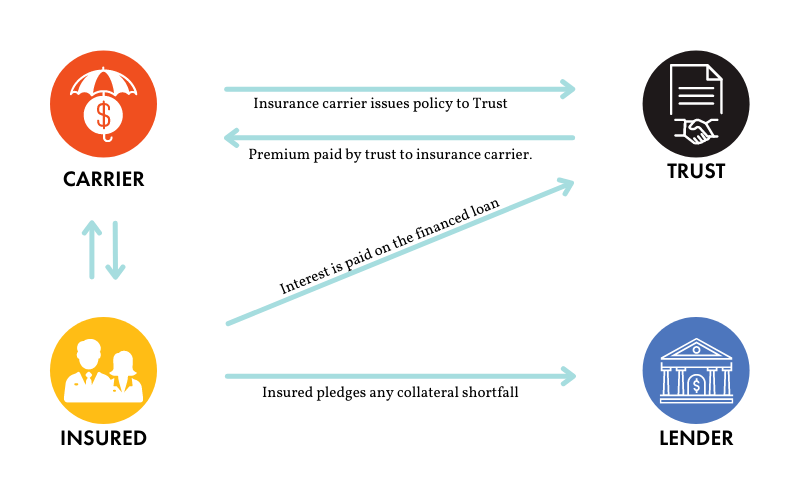

Those who are confident that premium financing is right for them typically set up an irrevocable life insurance trust (ILIT).

This trust is designed to own the life insurance policy, which means the policy is owned outside of your taxable estate. The beneficiaries receive the death benefit free of estate and income taxes. The ILIT would then take out a loan in order to pay the premiums. Typically, the policy is used as collateral. In the early years, the cash value of the policy will not be sufficient collateral for the loan — you may need to use a portion of your investment portfolio to make up the difference.

By funding the ILIT with a loan rather than direct contributions, you can limit your exposure to gift taxes and avoid exhausting your lifetime gift tax exclusion. Annual contributions to the ILIT may be needed to cover interest payments on the loan, but are typically less than the premium and may be within your annual gift tax exclusion limit.

Utilizing Premium Financing to Facilitate Wealth Transfer

John and Rebecca are a married couple in their 50s with three adult children. For the last 30 years, John has owned and operated a real estate development company, amassing a net worth of $30 million, much of which is illiquid and tied up in properties. They worry that their children may need to sell off some of their assets in order to pay the estate tax that will be due upon their death.

As John and Rebecca approach retirement, they are thinking more and more about how best to craft a tax-efficient estate plan so they can pass on their wealth to their children. When discussing their goals with their estate planning attorney, she explained the value of taking out life insurance policies to cover the tax expenses their estate would incur, and referred them to a number of insurance agents with the aim of finding the best policy for their particular situation.

Working with their estate attorney and an insurance professional, John and Rebecca determined the appropriate policy type and amount of death benefit required. Their insurance professional illustrated several options for acquiring the policy, including a short-pay and pay-for-life strategy. Rebecca and John preferred the idea of a short-pay strategy, but the relative premium created a cash flow concern. That’s when they turned to a private banker for advice.

The wealth manager and private banker recommended a loan that finances an annual $2 million premium payment for a period of 10 years to match the short-pay option, using the cash surrender value of the insurance policy and John and Rebecca’s $5 million investment account as collateral. As a result, they were able to support the structure without affecting their lifestyle. The couple worked with their estate planning attorney to set up an irrevocable life insurance trust that would hold the policy, and named their children as the trust beneficiaries.

By working with a team of experts, John and Rebecca were able to construct a strategy that would ensure that they are able to transfer their wealth to their children in the most efficient way possible, while still being able to pursue portfolio growth and minimize their taxes in the here and now.

Premium Financing is Not Risk Free

In addition to the tax efficiency of financing life insurance premiums, the ability to achieve a positive arbitrage between the interest rate of the loan and the crediting rate in the policy is foundational to any financing strategy. As long as the latter exceeds the former consistently over time, it’s possible that you may be able to repay the loan using just the cash value of the policy, while retaining enough cash in the policy to keep it in force through your life expectancy without having to pay additional premiums.

The flip side of this is that if interest rates rise faster than the policy performs, you may find yourself in a situation where the loan fails to fund your estate planning need, and surrender could create taxable income. While the cash values may be insufficient to support the outstanding loan balance, any gain in the policy would create taxable income, typically at ordinary income rates, if surrendered.

Premium financing is not a risk free strategy, and while it can provide tremendous benefits, it’s important to also appropriately identify the potential risks with your team of advisors.

Have an Exit Strategy

Setting up a premium financing strategy is only half the battle. You also need a thoughtful plan on how to get out of it when the time comes. Before you start down this path, work with your advisors to answer a few key questions:

- Why am I doing this? What is my goal?

- How will I know I’ve achieved that goal?

- What risks will I face and how will I react to them?

- How and when will I repay the loan?

- What other estate planning techniques may I need to employ?

The key to success is consistent monitoring. This strategy requires ongoing oversight and coordination by advisors who can assess both the performance of the policy and loan in concert with one another. When using leverage, even the smallest of changes to your strategy can have a significant effect on the outcome. Be sure your team has the expertise to help you along every step of your journey. Having a clear sense of your desired outcome will enable you and your advisors to properly design your premium financing strategy and provide you with a clear goal that governs any necessary adjustments down the road.

We make it easy,

so you can focus on

what's important.

English