Individual

Retirement

Plans

Individual Retirement Plan is much more than accumulating assets, it’s about connecting your wealth with your values so you can do what matters most to you. An important milestone for many people is their retirement day. It’s when you did it — you took care of business and accomplish the goal of an early retirement. However, when that day does come, without planning in advance, you could discover that it may not be all you expected. Planning early for your retirement can help make sure that your future is relaxing and fun-filled.

Whether you have already been thinking about retirement or not, planning for such a big change can be intimidating. Critical decisions such as how long to work, when to start Social Security, whether a Roth conversion makes sense for you and where to invest your money can make a huge impact on your retirement lifestyle. Through a series of meetings, we unpack visual frameworks to educate you on best practices in financial planning. We then begin to collaborate with you to link these frameworks to your financial circumstances so that you have projections that uniquely represent your circumstances and goals. This is what we like to call “client financial review (CFR).”

Process of Individual Retirement Planning

This process includes building a personal balance sheet, projecting retirement resources over time, linking your asset allocation to such projections and integrating your financial and estate plans.

With dozens of different inputs and assumptions, the CFR allows us to collaborate in changing the assumptions on the spot to show what might happen if your expenses, rates of return, pensions, cost of living adjustments, Social Security benefits, long-term care needs, legacy gifting goals or other inputs change.

As you engage in this collaborative process, you will have increasing confidence that you have considered a breadth of different potential scenarios and made choices that truly align your wealth with your values. Thereafter, regular updates of the plan ensure that you have a sense of your progress toward your goals and any important steps to taken as you continue to move forward with Individual Retirement Plans in your mind.

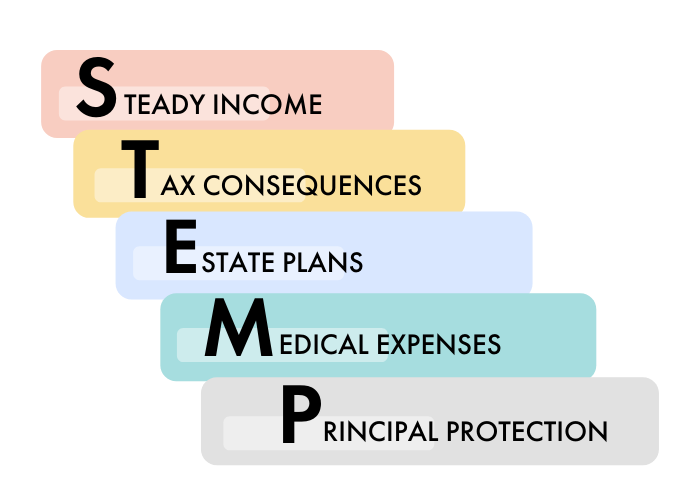

Five Principles of Retirement Plans: STEMP

Our Retirement Planning Steps:

- Step 1: Initial Client Financial Review (Money In & Out)

- Step 2: Financial Goal Setting

- Step 3: Planning with Time-frame

- Step 4: Individual Solutions & Applications

- Step 5: Review and Course Corrections (Annual Financial Review)

IRAs, a.k.a. Individual Retirement Account, allow you to make tax-deferred investments to provide financial security when you retire. Contributions you make to a traditional IRA may be fully or partially deductible, depending on your circumstances, and generally, amounts in your traditional IRA (including earnings and gains) are not taxed until distributed.

You can set up an IRA with a:

- bank or other financial institution

- life insurance company

- mutual fund

- stockbroker

For 2019, your total contributions to all of your traditional IRA cannot be more than: $6,000 ($7,000 if you’re age 50 or older), or your taxable compensation for the year, if your compensation was less than this dollar limit. The IRA contribution limit does not apply to:

- Rollover Contributions

- Qualified Reservist Repayments

Your traditional IRA contributions may be tax-deductible. The deduction may be limited if you or your spouse is covered by a retirement plan at work and your income exceeds certain levels.

You can’t make regular contributions to a traditional IRA in the year you reach 70½ and older. However, you can still contribute to a Roth IRA and make rollover contributions to a Roth or traditional IRA regardless of your age.

If you file a joint return, you may be able to contribute to an IRA even if you did not have taxable compensation as long as your spouse did. The amount of your combined contributions can’t be more than the taxable compensation reported on your joint return. If neither spouse participated in a retirement plan at work, all of your contributions will be deductible.

You can contribute to a traditional or Roth IRA whether or not you participate in another retirement plan through your employer or business. However, you might not be able to deduct all of your traditional IRA contributions if you or your spouse participates in another retirement plan at work. Roth IRA contributions might be limited if your income exceeds a certain level.

Traditional and Roth IRAs allow you to save money for retirement. This chart highlights some of their similarities and differences.

- You cannot deduct contributions to a Roth IRA.

- If you satisfy the requirements, qualified distributions are tax-free.

- You can make contributions to your Roth IRA after you reach age 70 ½.

- You can leave amounts in your Roth IRA as long as you live.

- The account or annuity must be designated as a Roth IRA when it is set up.

An annuity is a contract that requires regular payments for more than one full year to the person entitled to receive the payments (annuitant). You can buy an annuity contract alone or with the help of your employer.

Annuity Maximization for Individual Retirement

Do you hold an annuity and find you no longer need the income stream it can provide?

You may have used annuities as a savings vehicle as part of your financial plan. However, now you may find that you no longer need the money in the annuity and you want to pass the money on to your heirs. But did you know that the gains on your annuity (the portion that exceeds your original investment) will be taxable income to your heirs?1 In addition, the full value of your annuity is includible in your taxable estate, which could result in a diminished inheritance. By using life insurance to help maximize your annuity funds, you can provide your loved ones with the most value for your annuity funds, without the limitations of income or estate taxes.

Why Annuities for Retirement Plan?

We want you to make an informed decision when you consider the purchase of an annuity. Annuities are an excellent tool to help you plan for your financial security. Annuities offer a variety of benefits including tax-deferred growth, ability to avoid probate, and lifetime income.

Tax-deferred growth allows your money to grow faster because you earn interest on dollars that would otherwise be paid as taxes. Your principal earns interest, the interest compounds within the contract, and the money you would have paid in taxes earns interest. The chart to the right shows the impact of a tax-deferred annuity.

Annuities offer the ability to name a beneficiary, which may minimize the expense, delays, and publicity that comes with probate. Your named beneficiary may receive death proceeds as either a lump sum or monthly income.

Life Insurance Company can provide you with a guaranteed income stream with the purchase of a tax-deferred annuity. You have the ability to choose from several different income options, including life or a specific period. With non-qualified plans, a portion of each income payment represents a return of premium that is not taxable, reducing your tax liabilities.

Common Types of Annuities

Offers a declared fixed interest rate that is guaranteed for a specific period and guaranteed to never go below a specific percentage.

Interest rate credited to your annuity contract is linked to specific market indices that you can choose on an annual basis. Once the interest is credited you are guaranteed that it can never go down based on future market fluctuations.

Plan for retirement with a wide range of investment options, professional portfolio management, tax deferral, income options, and death benefits. Variable annuities can help increase your income for retirement and guarantee it lasts a lifetime.

Pay a fixed amount at regular intervals during an annuitant’s life, ending on his or her death.

Pay a fixed amount to the first annuitant at regular intervals for his or her life. After he or she dies, a second annuitant receives a fixed amount at regular intervals. This amount, paid for the life of the second annuitant, may be the same or different from the amount paid to the first annuitant.

A retirement annuity purchased by an employer for an employee under a plan that meets certain Internal Revenue Code requirements.

A special annuity plan or contract purchased for an employee of a public school or tax-exempt organization.

You are guaranteed an income stream ranging from a specific period of time to your entire life. An immediate annuity offers a solution to the problem of outliving your money.

Using Life Insurance to Help with Retirement Planning

Are you concerned about the financial security of your family today should something happen to you? Are you also uneasy about the future and falling short of retirement income? It may be time to consider life insurance. Take a moment to view our video about using life insurance to help with retirement planning.

Why Life Insurance for Retirement Planning

Permanent life insurance provides death benefit protection that can help you protect your loved ones in the future. Plus, it can be designed with the flexibility to address changing needs throughout your life. Life insurance can be a twofold strategy as part of your financial plan:

Death Benefit protection during working years

A solid financial plan often begins with life insurance. In the event of death, the proceeds are distributed to your beneficiaries generally income tax-free.

Potential source of funds to help support a longer retirement

Your premium payments on a permanent life insurance policy may accumulate cash value on a tax-deferred basis. Through policy loans and withdrawals, the cash value may then be used to help pay for a wide variety of needs in retirement. These could be planned distributions for planned expenses, or potential cash value may be used as additional funds to help protect you from outliving other retirement income sources or unplanned expenses. You may also access a portion of this death benefit during your lifetime in case of an unexpected illness. Cash value from your policy may be used for anything, from monthly cell phone bills to out-of-pocket co-pays to a favorite travel destination.

Example of Tax Issue

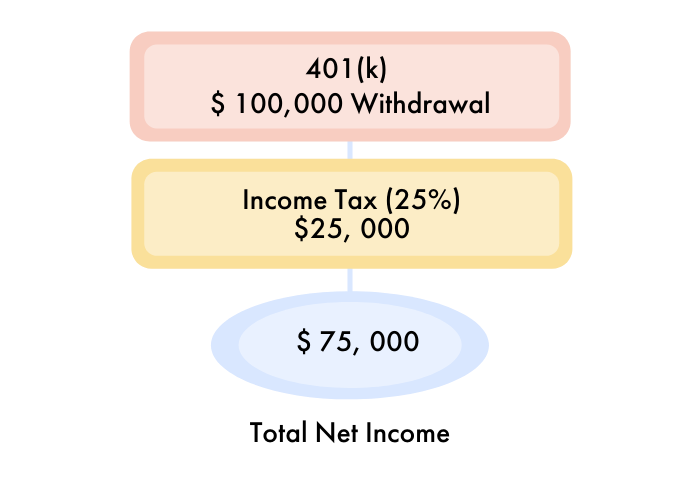

PROBLEM: 401(k) withdrawals are taxed as ordinary income [3]

In addition to some rental properties and his Social Security, Brian’s retirement plan consists only of his 401(k) plans. He has maximized his contributions and has a tidy sum saved. His financial professional (FP) points out that withdrawals from his 401(k) accounts will be taxed as ordinary income. His FP also explains that Brian may be in a higher tax bracket during retirement than he is now– due to possible changes in tax law and his growing account values. At retirement, assuming a 25% tax rate, an annual withdrawal of $100,000 would result in taxes of $25,000, leaving a net income of $75,000 available for his retirement.4 They discuss tax diversification as an option and that having some tax-free income would increase the amount available.

Example of Tax Issue

PROBLEM: 401(k) withdrawals are taxed as ordinary income [3]

In addition to some rental properties and his Social Security, Brian’s retirement plan consists only of his 401(k) plans. He has maximized his contributions and has a tidy sum saved. His financial professional (FP) points out that withdrawals from his 401(k) accounts will be taxed as ordinary income. His FP also explains that Brian may be in a higher tax bracket during retirement than he is now– due to possible changes in tax law and his growing account values. At retirement, assuming a 25% tax rate, an annual withdrawal of $100,000 would result in taxes of $25,000, leaving a net income of $75,000 available for his retirement.4 They discuss tax diversification as an option and that having some tax-free income would increase the amount available.

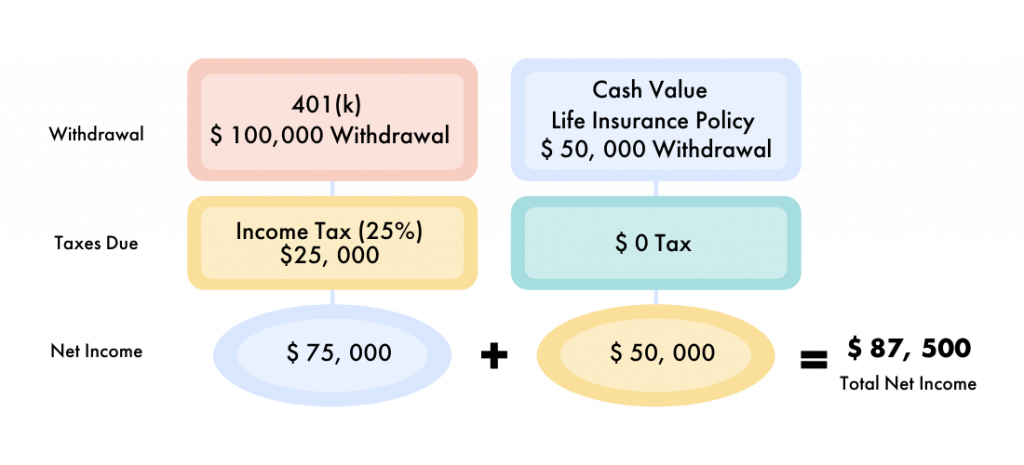

SOLUTION: Cash-value life insurance such as Indexed Universal Life Policy can help provide tax diversification.

Working with his FP, Charles has also decided that he needs $1 million of life insurance to protect the family. The FP shows Charles how a cash value life insurance policy can help him meet both objectives – life insurance protection for his family and a ‘taxed never’ asset to increase his diversification.

RESULTS: At retirement, Charles choose to take $50,000 from his 401(k) and from his cash value life policy. He was able to increase his net income by $12,500 over the 401(k)-only plan.

- The descriptions and features of the various assets in these tables are for general information purposes and address the most typical circumstances. There are many regulations governing the taxation and operation of all assets mentioned and you should seek the advice of a tax professional before making any changes to your current or future retirement plans, accounts or assets.

- Cash value life insurance policies are subject to Modified Endowment Contract rules that discourage overfunding based on face amount, insured’s age and other factors. Cash value life insurance also contains additional mortality charges that will increase the expense of this product. Also, distributions in excess of total premiums paid are taxable unless taken as loans (which are subject to interest charges). Consult a policy illustration for more information.

- This is a not an actual case. It is a hypothetical representation for illustrative purposes, only. The individual 401(k) plan and life insurance policy withdrawals are aggregated in the illustration for convenience. It is not a comprehensive analysis of the subject matter and you should work with a tax professional before making changes to your circumstances.

- Withdrawals are subject to federal tax of 25% and may be subject to state income taxes. A 10% federal early withdrawal tax penalty may apply if taken before age 59 1/2.

- Withdrawals in excess of total premiums paid are taxable unless taken as loans (which are subject to interest charges).

We make it easy,

so you can focus on

what's important.

English